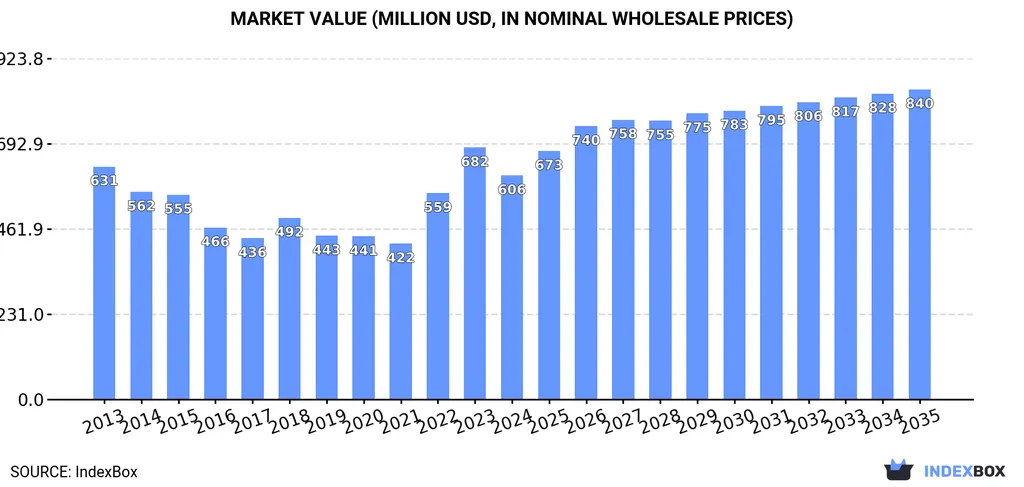

The Americas steel pipes market is poised for steady growth, with projections indicating a rise from USD 26.6 million in 2025 to USD 37.9 million by 2035, at a compound annual growth rate (CAGR) of 3.6%. This growth is underpinned by several key factors, including urbanization, government-backed infrastructure projects, and rising demand from the energy sector.

Manufacturers are increasingly focusing on enhancing product reliability through precision forming, heat treatments, and corrosion-resistant technologies. This shift towards technological advancements is crucial, as it not only meets sector-specific requirements but also aligns with evolving environmental regulations and sustainable practices. The oil and gas industry, in particular, is expected to be a significant revenue driver, especially with the discovery of unconventional sources and techniques like shale and fracking.

The dominance of carbon steel in the market is noteworthy, accounting for 54.2% of market revenue by 2025. Its high strength, cost efficiency, and adaptability make it indispensable for construction, oil & gas, and infrastructure applications. The construction sector, leading the end-use segment with 47.8% of total market revenue, drives consistent demand for steel pipes in structural support, plumbing, water distribution, and sewage management.

Seamless steel pipes, preferred for their mechanical strength and high-pressure resistance, represent 58.6% of revenue in 2025. Their extensive use in oil & gas, power generation, and water distribution underscores their reliability and cost efficiency. North America, particularly the U.S., dominates the market, with the U.S. holding 70.4% of the total share. Brazil, Canada, and Mexico also show steady adoption trends, making the region strategically important for manufacturers.

Despite these positive trends, the market faces challenges from high installation costs and competition from alternative materials like plastic and iron. Large-diameter pipes, in particular, remain expensive, limiting their application in specific sectors. Manufacturers must focus on innovation and cost efficiency to maintain competitiveness.

Key market players, including American Cast Iron Pipe Company, Baosteel Group, and Evraz Plc, are investing in R&D, production efficiency, and geographical expansion to gain a competitive edge. Strategic partnerships and sustainable practices are driving market differentiation and long-term growth.

The future outlook for the Americas steel pipes market is promising, with a focus on automation, R&D, and sustainable production. Short-term strategies include efficiency and automation, while medium-term priorities involve advanced technology adoption. Long-term goals center on sustainable manufacturing and environmental compliance.

This growth trajectory has significant implications for the sector. The increasing demand for durable, cost-effective, and corrosion-resistant steel pipes will likely spur innovation in manufacturing processes and materials. Government incentives and energy distribution projects will further enhance market opportunities, driving investment in infrastructure and energy sectors.

Moreover, the shift towards sustainable practices and eco-friendly production will shape the market’s future. Companies that prioritize environmental compliance and sustainable manufacturing will likely gain a competitive advantage. The adoption of advanced technologies, such as AI-driven manufacturing, will also play a crucial role in enhancing efficiency and quality.

In conclusion, the Americas steel pipes market is set for steady growth, driven by infrastructure modernization, energy sector expansion, and technological adoption. The sector’s future will be shaped by innovation, sustainability, and strategic investments, positioning it for long-term success.